Industrial Insurance Claim: A Comprehensive Guide for Manufacturing Facilities Recovering From Major Losses

.svg)

Understanding Industrial Insurance Claims After Major Facility Damage

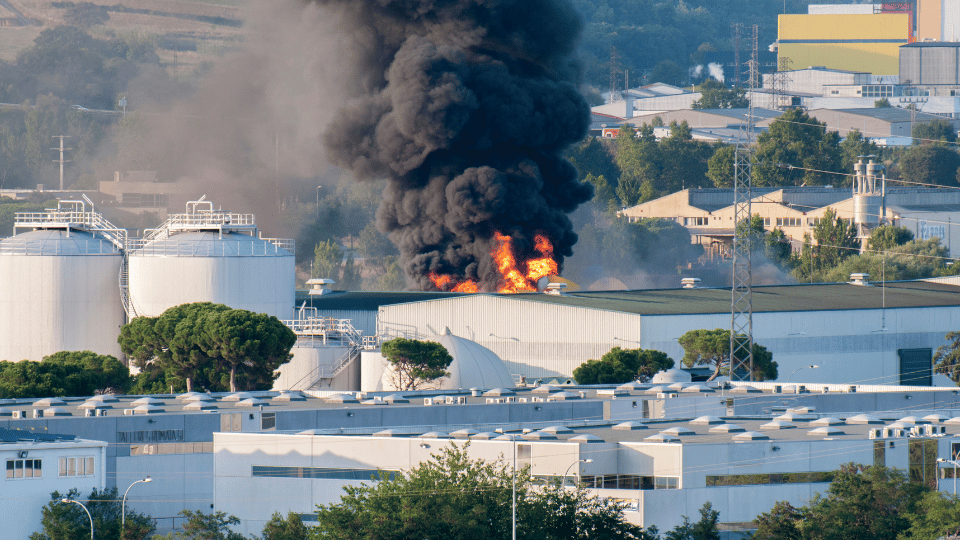

Industrial properties operate on a scale far beyond residential or commercial buildings. Factories, warehouses, distribution centers, processing plants, and manufacturing facilities are filled with systems that must work together flawlessly—machinery, robotics, conveyor systems, compressed air lines, electrical grids, heavy-duty HVAC units, sprinkler systems, production equipment, and specialized flooring. When damage occurs, it doesn’t just affect the building—it disrupts production, inventory, workflow, and revenue.

An industrial insurance claim becomes complex the moment the loss occurs. Damage to a single electrical panel can shut down an entire production line. A fire inside one section of a warehouse can contaminate a full shipment of goods with smoke and soot. Water from a burst line can damage raw materials, machinery controllers, sensors, and safety equipment. Even a minor storm event can compromise structural beams, cranes, or rooftop units.

Insurance companies know industrial losses are expensive. They often begin assessing the claim with a conservative approach, looking for ways to classify damage as wear-and-tear, maintenance issues, or unrelated to the event. Many industrial policyholders are surprised to discover insurers pushing responsibility onto subcontractors, equipment warranties, or internal safety protocols. Without strong documentation and a properly structured claim, facilities risk major financial losses and production downtime.

The stakes are much higher in industrial environments because every hour lost directly impacts the company’s ability to operate. A well-prepared industrial insurance claim is not just about repairing damage—it’s about protecting business continuity, equipment investments, and long-term output.

Why Industrial Damage Is Difficult to Document Without Expert Guidance

Industrial environments contain systems that the average insurance adjuster is not trained to assess. Most adjusters are familiar with homes and small businesses—but few have the experience required to understand how production equipment, robotics, electrical control centers, manufacturing lines, and specialized machinery interact. This knowledge gap leads to under-documentation, misinterpretations, and undervaluation of damage.

For example, insurance adjusters may photograph surface-level water damage but miss moisture inside machine housings or electrical panels. They may overlook structural stress on steel support beams caused by extreme heat. They may assume equipment is operational simply because it powers on—while ignoring calibration drift, sensor failure, belt misalignment, lubrication contamination, or internal component warping. These hidden issues can shut down production for weeks.

Proper documentation requires experts who understand industrial systems, including engineers, mechanical specialists, electricians, and industrial loss consultants. They evaluate damage with precision:

- Testing and diagnostics on machinery

- Thermal imaging on electrical systems

- Moisture mapping inside walls and mechanical areas

- Structural assessments of beams, rafters, and load-bearing components

- Evaluation of inventory contamination

- Review of safety hazards created by the incident

Insurance companies rarely conduct this level of assessment unless forced to do so. Without expert documentation, they may approve only superficial repairs—leaving the facility to cover the costly mechanical, structural, or operational failures that appear later.

Industrial insurance claim support ensures the full scope of damage is recorded early, accurately, and in a way the insurer must acknowledge.

Why Insurance Companies Push Back on Industrial Property Damage Claims

Industrial claims carry some of the largest potential payouts in property insurance. Repairing damaged equipment, replacing inventory, and addressing structural issues can quickly reach six or seven figures. Additionally, business interruption losses—lost revenue due to production downtime—often exceed the cost of physical damage itself.

Because of this, insurers intensify scrutiny on industrial claims. Common insurer strategies include:

They may claim that machinery failure was caused by poor maintenance rather than the covered event. They may argue that a production line that shut down due to electrical damage is “still operational” because parts of it still power on. They often classify contamination, corrosion, or internal component damage as pre-existing. They may try to replace only one part of a system, even if the entire line must be synchronized to work properly. They sometimes underestimate the cost of specialized labor, steel fabrication, or custom equipment installation.

Insurers also closely evaluate business interruption claims. They may argue that the facility could have continued running at partial capacity, even when this is impossible due to safety regulations or equipment dependencies. They may push back on projected revenue losses, replacement timelines, or the cost of temporary solutions.

Industrial insurance claim experts understand these tactics and prepare counter-evidence before the insurer attempts to minimize the claim. Their goal is to keep the facility financially protected during recovery—not leave the business absorbing losses that should have been covered.

How Industrial Insurance Claim Professionals Protect Manufacturers and Large Facilities

When industrial damage occurs, the facility needs more than simple claim filing—they need full-scale claim management. Professional claim support provides the structure, documentation, and technical knowledge necessary to secure full compensation.

Industrial claim specialists work to:

- Conduct complete assessments of machinery, structural elements, and production systems.

- Verify hidden mechanical and electrical issues that insurers often overlook.

- Manage communication with the insurer to prevent delays or misinterpretations.

- Prepare detailed reports that explain the technical nature of the damage.

- Challenge incomplete or undervalued estimates.

- Ensure business interruption calculations reflect real production losses.

- Advise on temporary solutions that preserve workflow and safety.

Most importantly, they understand how industrial facilities work. They do not treat machinery as simple assets—they analyze operational dependencies, throughput, calibration needs, software controls, and the relationships between equipment and building systems.

Their work ensures that the facility is not pushed into accepting partial repairs, unsafe operation, or incomplete settlement payouts. Instead, they create a claim strategy that restores the entire operational environment—machinery, structure, workflow, and production capacity.

Conclusion

Industrial insurance claims are complex, high-stakes cases that require specialized knowledge and strong evidence. Manufacturing facilities, warehouses, and large industrial properties cannot rely on basic inspections or incomplete assessments. Damage spreads into structural components, machinery systems, inventory, and workflow in ways that insurance companies often fail to recognize or acknowledge.

With professional industrial insurance claim support, facilities gain an advocate who understands both the technical and financial impact of industrial losses. This ensures accurate documentation, fair valuation, and a claim strategy focused on restoring full operational capability. Instead of navigating overwhelming insurance processes alone, businesses gain the expertise needed to rebuild stronger and minimize downtime.

.svg)