Storm Claim Assistance: A Complete Guide for Homeowners Recovering After Severe Weather Damage

.svg)

Why Storm Claim Assistance Is Essential After Severe Weather Events

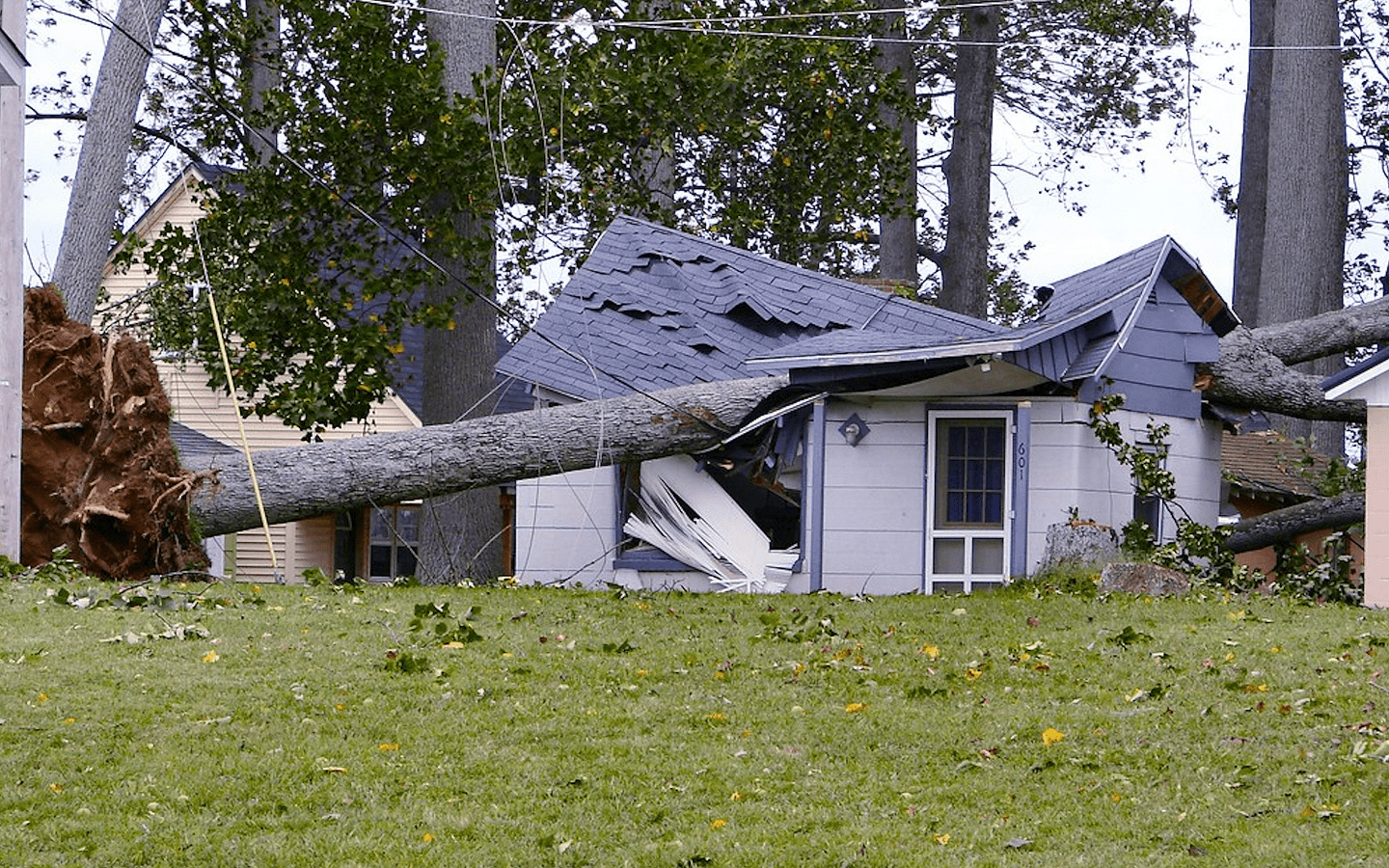

Storms are among the most destructive forces a home can face. Whether it’s wind tearing at the roof, hail shattering shingles and siding, or heavy rain flooding interior spaces, storm damage often compounds rapidly. What begins as a few missing shingles or a small leak can quickly turn into widespread structural issues that threaten the home’s integrity. Unfortunately, the insurance claim process rarely matches the urgency or complexity of the situation.

Storm damage is uniquely challenging because it involves multiple types of loss occurring at once. A single storm can cause roof damage, siding cracks, broken windows, gutter failures, fence collapse, fallen trees, interior water intrusion, and electrical problems. Insurance companies struggle to categorize these damages cleanly, often separating them into different claim sections or questioning whether all the issues were caused by the same event. This confusion frequently leads to disputes, delays, and partial payments.

Homeowners often assume that visible surface damage tells the full story, but storm impact is deeper and more unpredictable. Wind uplift may break the shingle seal even when the roof appears intact. Rain can seep behind siding, creating hidden moisture pockets that later turn into mold. Hail impacts can fracture roofing material below the surface, weakening it even when the top layer looks unscathed. Many of these issues are invisible without specialized tools and a trained eye.

The emotional toll further complicates things. After a major storm, homeowners must balance temporary repairs, safety concerns, family needs, and insurance communication—all at once. Trying to manage this while navigating complex policy language and insurer requirements is overwhelming. Storm claim assistance provides clarity during chaos, helping homeowners avoid mistakes that could cost thousands of dollars in denied or underpaid claims.

How Storm Claim Assistance Helps Identify and Document Hidden Damage

A successful storm claim depends heavily on documentation—far more than most homeowners realize. Insurance companies rely on precise evidence, timestamps, and detailed reporting to determine what damage is covered and how much will be paid. If the evidence is incomplete or not professionally structured, insurers may argue that part of the damage occurred before the storm or is unrelated.

Storm claim assistance starts with a thorough, systematic inspection of the property. This goes far beyond a basic visual check. Specialists examine the roof slope by slope, checking for lifted shingles, broken seals, impact marks, displaced ridge caps, and underlayment tears. They inspect siding for cracks, punctures, warped boards, and areas where wind-driven rain may have infiltrated. Windows and doors are checked for pressure damage, frame misalignment, or hidden air leaks.

Interior inspections are equally important. Moisture mapping tools detect hidden water trapped behind walls, under flooring, or inside insulation. Thermal cameras reveal temperature variations that indicate structural moisture. These tools prevent insurers from claiming that the damage is superficial or unrelated to the storm.

Detailed photographs, high-resolution drone imagery, written observations, and contractor-backed repair estimates all become part of a powerful evidence package. This level of documentation closes loopholes insurers often use to lower payouts. It ensures the claim accurately reflects the true cost of restoring the home—not just the visible damage.

Why Insurance Companies Undervalue Storm Claims — and How Assistance Protects You

Storm damage claims are among the most frequently underpaid claims in the insurance industry. This happens largely because insurers try to limit their exposure when storms affect entire neighborhoods. A single major storm can result in thousands of claims at once, placing pressure on insurers to minimize payouts.

One method insurers use is labeling significant damage as “cosmetic.” They may claim that dents in metal roofing, siding impressions, or gutter bending don’t affect functionality—even when these issues clearly compromise long-term performance. Another tactic is attributing roof problems to age instead of the storm. Homeowners often lack the expert knowledge to counter these arguments, making it easy for insurers to justify low settlements.

Insurers also rely on rushed inspections. After widespread storms, company adjusters may inspect dozens of homes per day, often spending less than ten minutes on each. This leads to missed damage, incomplete reports, and lowball estimates. When homeowners provide little evidence, insurers take advantage of the information gap.

Additionally, depreciation is frequently miscalculated. Even when a homeowner has full replacement cost coverage, insurers initially apply heavy depreciation, putting the burden on the homeowner to complete repairs before receiving full compensation. Without understanding how depreciation works or how to challenge improper calculations, homeowners accept smaller payments than they deserve.

Storm claim assistance prevents these pitfalls. Professionals counter inaccurate reasoning using code requirements, industry repair standards, and precise documentation. They challenge low offers, identify missing line items in the insurer’s estimate, and ensure every storm-related repair is properly included.

How Storm Claim Specialists Strengthen Negotiations and Settlement Outcomes

Negotiating a storm claim is a complex process that requires expertise, evidence, and persistence. Homeowners often feel pressured to accept the insurer’s initial offer because they don’t know what a fair settlement looks like. Storm claim specialists step in to act as advocates, ensuring the negotiation process is balanced and fair.

They begin by comparing the insurer’s estimate with real-world contractor pricing. Insurance estimates often use outdated or incomplete pricing databases that don’t reflect local labor or material costs. Specialists create a comprehensive, accurate estimate that includes everything required to restore the home to pre-storm condition: roofing materials, underlayment, flashing, siding, windows, insulation, structural repairs, interior restoration, and more.

When discrepancies arise, specialists provide detailed explanations backed by building codes, manufacturer installation guidelines, and local market standards. This evidence makes it extremely difficult for insurers to justify lowball settlements.

Storm claim professionals also handle all communication with the insurance company. They manage paperwork, deadlines, and negotiations, preventing accidental statements that could weaken the claim. Their experience puts pressure on insurers to act fairly, follow policy language, and comply with state insurance guidelines.

The result is typically a faster, more accurate settlement—one that fully accounts for the damage and ensures long-term protection for the home.

What Homeowners Should Do After a Storm to Strengthen Their Claim

The actions taken immediately after a storm significantly influence the success of a claim. Homeowners should begin by inspecting the property for obvious signs of damage such as missing shingles, broken branches, shattered windows, or interior leaks. Even if damage appears minor, it’s important to document everything.

Photos and videos should be taken before any cleanup or repairs begin. This includes both close-up details and wide-angle views. Documentation should cover all affected areas—roof, siding, gutters, landscaping, fences, windows, and interior surfaces.

Temporary repairs may be necessary to prevent further damage, such as covering openings or removing water, but they must be documented beforehand to avoid disputes with the insurer. All receipts for emergency services, tarping, or materials should be saved, as many policies reimburse these expenses.

Homeowners should be careful when speaking with the insurance company. Casual statements about the severity of the damage, the age of the roof, or assumptions about what caused the issue can be used against them later. It is always best to speak factually and rely on professional guidance whenever possible.

Requesting a thorough professional inspection early ensures hidden damage is not overlooked. This helps create a clear and defensible claim from the start.

Conclusion

Storm claim assistance is one of the most valuable resources a homeowner can rely on after severe weather. Storm damage is complex, often hidden, and frequently underestimated by insurers. A storm claim specialist provides clarity, evidence, negotiation strength, and peace of mind. They ensure every part of the damage is identified, documented, and fully compensated.

With expert support, homeowners avoid underpayments, rushed inspections, and denied items—ultimately achieving a fair settlement that restores the home to its pre-storm condition.

.svg)