Wind Damage Adjuster: How Homeowners Benefit From Professional Help After Severe Wind Events

.svg)

Why Wind Damage Is Hard for Homeowners to Recognize and Prove

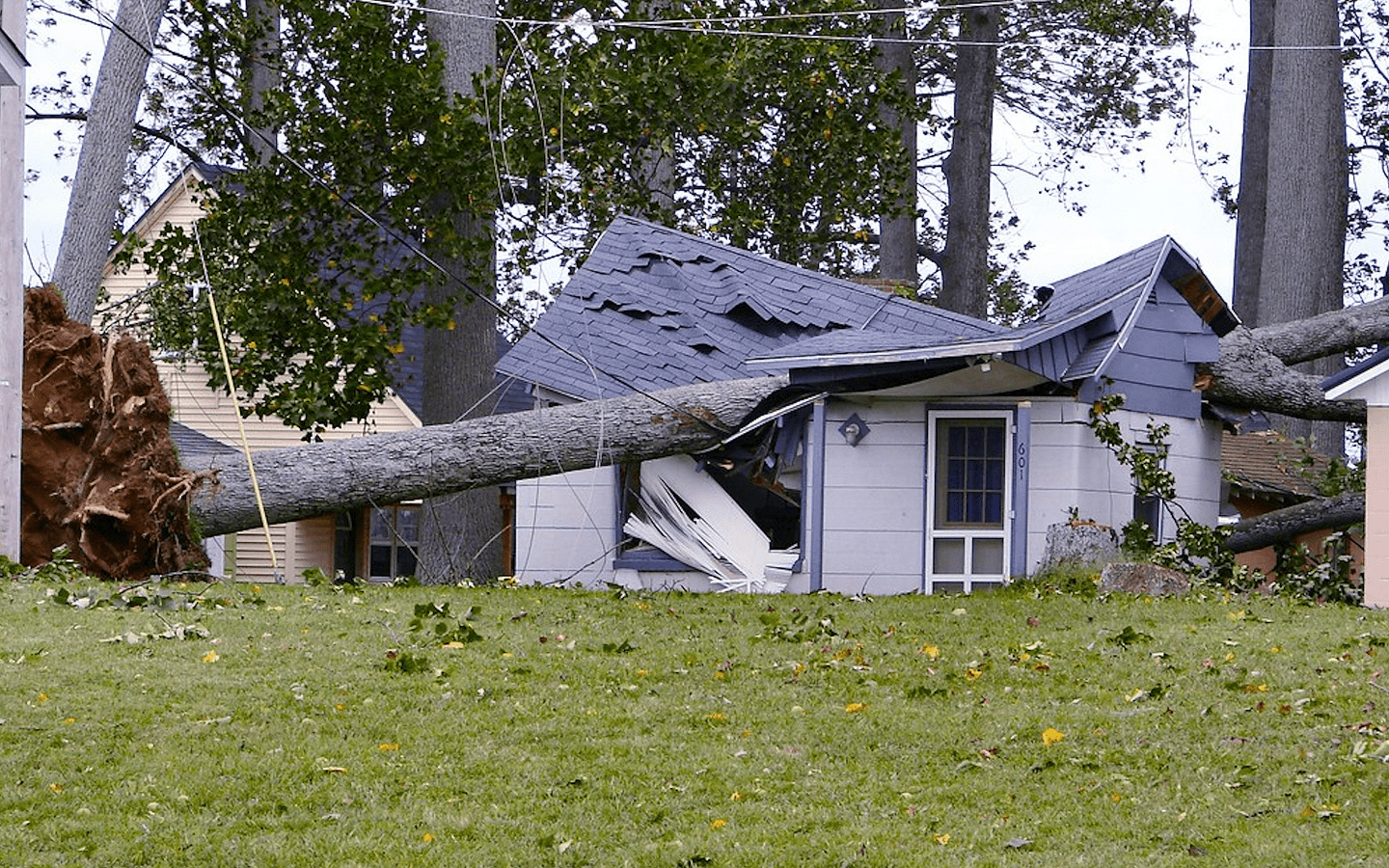

Wind damage is one of the most misunderstood forms of property loss. Unlike hail or fire, wind rarely leaves a single obvious point of impact. Instead, it creates subtle but significant structural changes—lifting shingles, loosening fasteners, cracking siding, bending gutters, and compromising the building envelope. Many of these issues cannot be seen from the ground, and some remain hidden until rainwater begins to seep inside. This delayed appearance of damage often causes disputes with insurance companies.

Homeowners may assume that if the roof looks mostly intact, no major damage occurred. In reality, wind uplift can break the seal between shingles and underlayment, leaving the roof vulnerable to leaks during the next storm. The same applies to siding, window seals, and flashing. Wind weakens materials gradually, creating openings for water intrusion without obvious visual clues. Insurance companies know this and frequently argue that the damage was minimal, cosmetic, or unrelated to the windstorm.

Another challenge is that windstorms vary in direction and intensity. One side of the home may be heavily impacted while another appears untouched. Without professional knowledge, homeowners cannot easily explain these patterns to an insurance adjuster. Insurers often rely on this lack of clarity to minimize claims. Even when the damage is clearly storm-related, many adjusters classify it as normal aging, wear and tear, or deferred maintenance.

Emotionally, wind damage creates uncertainty. Homeowners may feel anxious about hidden leaks, long-term moisture, and potential mold growth. They worry about missing something important or accepting an insurance payment that is too low to cover real repair costs. Not knowing the true extent of the damage—and not knowing how to properly present it to insurance—leaves many homeowners vulnerable during the claims process.

A wind damage adjuster eliminates this uncertainty by identifying, documenting, and proving every aspect of the loss.

How a Wind Damage Adjuster Properly Evaluates Roof, Siding, and Exterior Damage

A wind damage adjuster begins with a comprehensive inspection designed to uncover damage that homeowners and insurance adjusters often overlook. This is not a quick walkthrough. It is a detailed, methodical evaluation that focuses on structural integrity, moisture exposure, and safety.

Wind damage adjusters climb the roof, inspect each slope, and physically check shingle adhesion. They look for lifted shingles, broken seals, displaced ridge caps, exposed nails, and underlayment tears. These conditions are not always visible from the street, and many insurance adjusters skip this hands-on inspection—leading to incomplete or inaccurate reports.

The adjuster also reviews siding for cracks, lifted panels, and impact points where debris struck at high speed. Windows and doors are checked for compromised seals, frame separation, and stress fractures. Gutters and downspouts are inspected for bending, detachment, and blockages caused by wind-driven debris. Even minor-looking damage can compromise the functionality of the home and lead to long-term moisture problems if not addressed.

Moisture mapping plays a critical role. Using thermal cameras and moisture meters, a wind damage adjuster identifies water that has entered the structure through openings created by the storm. This hidden moisture is one of the biggest threats to a home’s safety and value. If moisture is not discovered and addressed quickly, it leads to mold, rot, and structural deterioration. Insurance companies often overlook this key factor, but a professional report ensures it is included in the scope of repairs.

The final inspection report includes high-resolution photos, professional measurements, moisture readings, and detailed notes. This becomes the homeowner’s strongest evidence during negotiations and is essential for preventing insurers from downplaying or denying parts of the claim.

Why Insurance Companies Often Undervalue Wind Damage Claims

Insurance companies frequently push back on wind damage claims because the damage is often subtle, complex, and easy to dispute. Unlike hail impacts or fire destruction, wind-related issues require expertise to identify and quantify. This gives insurers an opportunity to reduce payouts by challenging the cause or severity of the damage.

One tactic insurers use is labeling the damage as “cosmetic.” They may claim lifted shingles, cracked siding, or bent gutters are purely aesthetic and do not affect the structure. In reality, these issues often create immediate vulnerabilities that can lead to water intrusion and costly long-term repairs.

Another common approach is attributing the damage to aging or prior wear. If the roof is older, insurers may argue the shingles were already weak, ignoring the fact that wind uplift can compromise even newer roofing systems. Without proper evidence, homeowners struggle to disprove these claims.

Some adjusters conduct extremely short inspections—sometimes as little as five minutes—ignoring hidden damage and providing incomplete reports. These rushed assessments lead to low estimates that fail to cover real repair needs. Homeowners who are unaware of the true scope of damage often accept the insurer’s assessment simply because they lack the expertise to challenge it.

Improper depreciation is another major issue. Even when policies provide replacement cost coverage, insurers often apply heavy depreciation upfront, pressuring homeowners to accept smaller payments. A wind damage adjuster helps ensure depreciation is applied correctly—or not at all—according to the policy.

Having a professional advocate prevents insurers from using these tactics to undervalue or deny legitimate claims.

How a Wind Damage Adjuster Strengthens Your Insurance Claim

A wind damage adjuster acts as the homeowner’s dedicated advocate throughout the entire claims process. Their goal is simple: to ensure the insurance company pays for every repair required to restore the home to pre-loss condition.

They begin by documenting the true extent of the damage using industry-standard tools and methods. Their reports include detailed evidence that insurers cannot easily dispute. These reports follow insurance guidelines and are formatted in a way that aligns with how insurance companies evaluate claims. This makes the adjuster’s findings incredibly impactful during negotiations.

The adjuster also prepares accurate repair estimates based on real contractor pricing in the homeowner’s area. These estimates include labor, materials, code upgrades, structural repairs, and necessary replacements. Insurance estimates are often incomplete, outdated, or intentionally minimized. A professional counter-estimate forces the insurer to reevaluate their position.

Communication and negotiation are major strengths of a wind damage adjuster. They handle all discussions with the insurer, ensuring homeowners avoid unintentional statements that could weaken the claim. They challenge lowball offers, correct errors in the insurer’s assessment, and escalate disputes when necessary. Homeowners often receive significantly higher settlements simply because they have someone fighting on their behalf.

Finally, a wind damage adjuster ensures insurance companies follow the policy correctly. Many homeowners do not fully understand their coverage, deductibles, exclusions, or rights. Professionals interpret the policy accurately and ensure the insurer honors its obligations.

What Homeowners Should Do Immediately After Suspecting Wind Damage

The steps homeowners take after a windstorm can greatly affect the outcome of their claim. Acting quickly and strategically helps protect both the home and the claim.

Homeowners should begin by visually checking for signs of damage such as missing shingles, fallen branches, cracked siding, or interior leaks. Even if damage is not obvious, the roof and exterior should be inspected by a professional. Hidden wind uplift often goes unnoticed until it causes secondary water intrusion.

Documenting early evidence is critical. This includes photos, videos, and written notes about the time and severity of the storm. These details help establish a clear timeline for the claim.

Homeowners should also take steps to prevent additional damage. Covering exposed areas, removing debris, and cleaning up water intrusion are important, but the scene should be documented before these temporary repairs occur. Insurers may deny parts of the claim if they believe the homeowner failed to mitigate additional damage.

All receipts—for emergency services, temporary housing, or materials—should be saved. Many policies reimburse these expenses under additional living or emergency repair provisions.

Most importantly, homeowners should be cautious about discussing the claim with the insurance company before understanding the full scope of damage. Early statements can be used to limit coverage, especially if the homeowner unknowingly downplays the severity of the situation.

Conclusion

Wind damage often appears minor at first glance, but the impact can be far more extensive than homeowners realize. Subtle structural shifts, hidden moisture, and compromised roofing components can lead to long-term damage if not identified and properly repaired. Unfortunately, insurance companies frequently undervalue wind claims, relying on rushed inspections and technical arguments to minimize payouts.

A wind damage adjuster helps homeowners overcome these challenges by providing detailed inspections, strong documentation, accurate repair estimates, and skilled negotiation. With expert support, homeowners can secure fair compensation, restore their property fully, and protect themselves from long-term structural problems.

When severe wind strikes, having the right advocate on your side makes the difference between a stressful claim and a successful recovery.

.svg)