Storm Damage Insurance Claim Help: A Complete Guide for Homeowners Facing Wind, Debris, and Structural Loss

.svg)

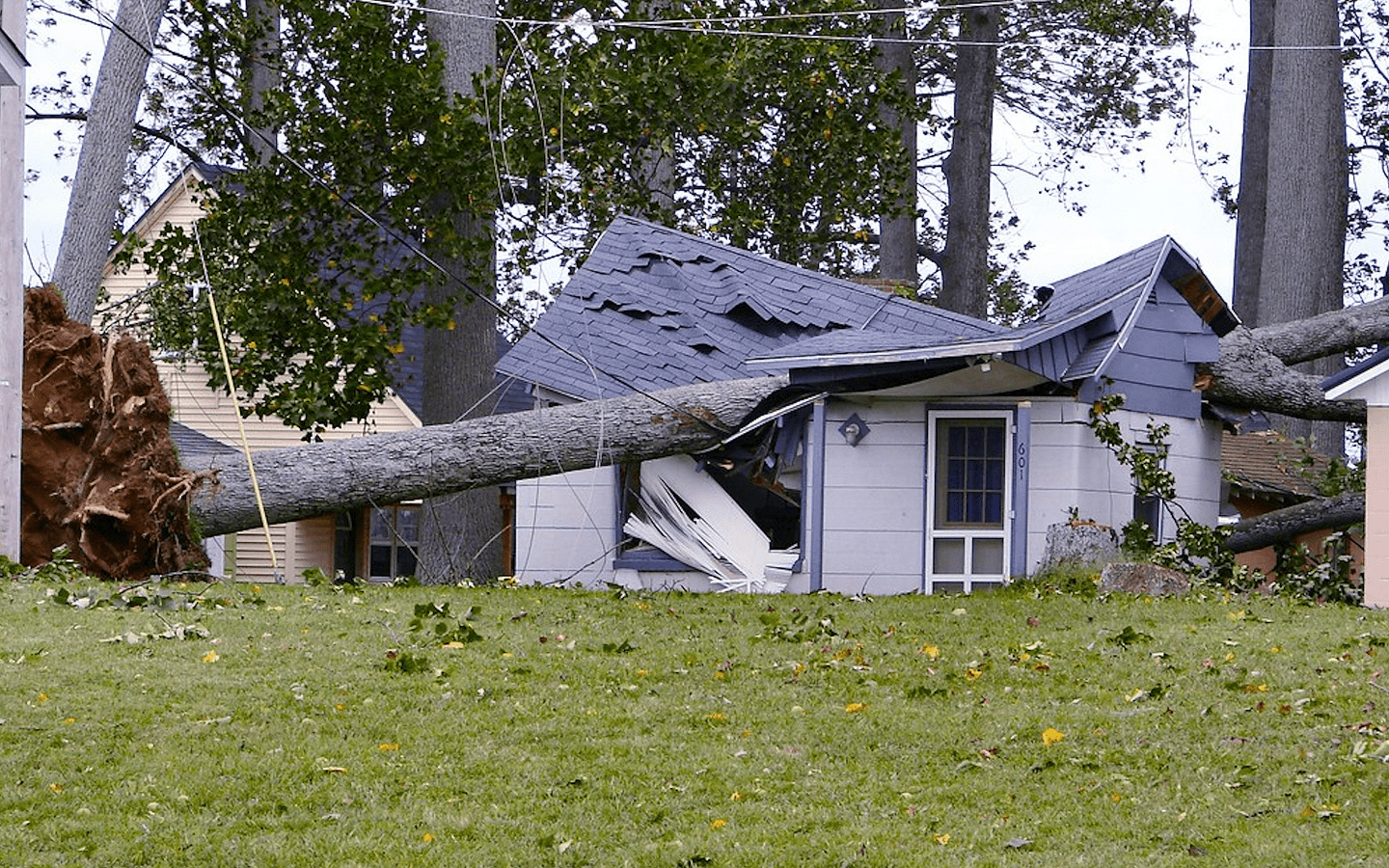

Why Storm Damage Insurance Claims Are Difficult for Homeowners

Storms are unpredictable, destructive, and fast. Within minutes, strong winds, flying debris, falling branches, and heavy rain can tear apart roofing systems, damage siding, shatter windows, and expose the home to extensive water intrusion. After the chaos settles, homeowners are left staring at structural problems, safety hazards, and uncertainty about what their insurance will actually cover. Filing a storm damage insurance claim might seem simple, but the process is far more complicated than most people expect.

The biggest challenge begins with the nature of storm damage itself. Storm impact is rarely uniform—one part of the roof might be ripped open while another appears untouched. Wind can lift shingles without fully detaching them, leaving homeowners unaware of the hidden exposure. Siding may look intact but have cracks that allow moisture inside. Windows may seem stable but have compromised seals. What appears on the surface is rarely the full scope of the loss.

Insurance companies take advantage of this complexity. Storm claims are some of the most frequently underpaid claims in the industry because insurers often argue that damage is cosmetic, minimal, or unrelated to the storm. They may claim shingles were “already brittle,” siding damage was “pre-existing,” or interior moisture was caused by “maintenance issues” rather than the storm itself. These tactics help insurers reduce payouts, shifting major repair costs back to the homeowner.

Another challenge is volume. After a major storm, thousands of claims arrive at the same time. Insurance companies are overwhelmed, meaning adjusters often rush inspections and overlook critical details. Some inspections last less than ten minutes, even when the home has multiple areas of impact. Homeowners rely on these adjusters to accurately assess damage—but the reality is that many storm inspections are incomplete or significantly undervalued.

Emotionally, the experience is exhausting. Storm damage disrupts routines, forces families to relocate, and leaves homeowners dealing with temporary repairs, safety risks, and uncertainty about long-term structural issues. Navigating a storm damage insurance claim in the middle of all this stress can be overwhelming. Understanding the process—and knowing how to defend your rights—is essential for achieving a fair outcome.

How to Document a Storm Damage Insurance Claim the Right Way

Documentation plays an enormous role in determining how much homeowners receive from insurance companies. Storm damage is often widespread but subtle, and insurers rely on clear proof to justify every dollar they pay. When documentation lacks detail, insurers fill in the gaps in their favor—not the homeowner’s.

The first step is capturing wide-angle photos of the entire property, including the roof, siding, windows, gutters, fences, and yard. After storms, debris patterns help show the direction and force of the wind, which can prove how damage occurred. Close-up photos of torn shingles, dents, cracks, broken tree limbs, and any interior water intrusion show the severity of the impact.

Homeowners should also document the condition of personal belongings damaged by rain, wind, or structural openings. Furniture, electronics, flooring, clothing, and appliances may need to be inventoried with detailed descriptions and approximate values. Without a complete list, insurers often exclude or undervalue these items.

Professional inspections make documentation significantly stronger. Storm damage experts use moisture meters, thermal imaging, drone photography, and code-based repair standards to create detailed reports. These evaluations reveal hidden damage that homeowners—and sometimes even insurance adjusters—cannot detect on their own. Wind-lifted shingles, compromised underlayment, waterlogged decking, or damaged structural elements might not be visible from the ground but can drastically affect the home’s safety.

Repair estimates are also essential. Insurance companies frequently submit their own estimates using outdated pricing or incomplete scope descriptions. A professional estimate based on local contractor rates ensures the insurer doesn’t undervalue labor, materials, or required code upgrades. The more detailed the documentation, the harder it becomes for insurers to deny or minimize the claim.

Why Insurance Companies Undervalue Storm Damage Claims

Storm damage insurance claims are some of the most aggressively disputed claims in the industry. The reason is simple: storms create large-scale losses, and paying every claim fully would cost insurers millions. To minimize financial exposure, insurance companies rely on specific tactics to reduce payouts.

One of the most common strategies is claiming the damage is cosmetic. Insurers often argue that dents in metal, cracked siding, or lifted shingles don’t affect the functionality of the home. However, cosmetic damage can lead to long-term deterioration, moisture intrusion, and structural issues. Claiming it is “non-functional” allows insurers to avoid paying for full replacements.

Another tactic is applying improper depreciation. Even when homeowners have replacement cost coverage, some adjusters heavily reduce payouts upfront, pressuring homeowners to accept lower settlements. Many homeowners don’t realize that replacement cost policies often require additional steps to recover full value.

Insurers also blame pre-existing conditions. They may argue that the roof was already old, shingles were brittle, or siding cracked before the storm. Without strong documentation, these claims can be difficult to dispute—even when incorrect.

Additionally, insurance adjusters frequently overlook hidden damage. Quick walk-throughs or drive-by assessments fail to capture moisture behind walls, underlayment damage, or structural weakening. Rushed inspections result in incomplete claim scopes, leaving homeowners with repairs far exceeding the insurer’s initial estimate.

Understanding these tactics helps homeowners recognize when the insurer is minimizing the claim and when to seek expert assistance.

How Professionals Strengthen a Storm Damage Insurance Claim

Storm damage claim professionals, including public adjusters and storm restoration specialists, play a critical role in helping homeowners secure fair settlements. Their expertise comes from handling claims daily, understanding policy language, and recognizing damage patterns that insurers often overlook.

A professional begins with a full inspection—not the quick, surface-level review insurers often conduct. They examine the roof, attic, walls, windows, foundations, and exterior structures using tools that detect hidden moisture, structural shifts, or subtle impact marks. This comprehensive approach ensures that every part of the damage is captured and documented.

Next, professionals prepare detailed repair estimates based on industry standards, code requirements, and local market pricing. Insurance adjusters sometimes use outdated software or minimal cost assumptions that underestimate the true cost of repairs. A professional estimate forces the insurer to reevaluate their numbers and justify any discrepancies.

Professionals also manage communication with the insurer, preventing homeowners from being pressured into accepting low offers. They handle disputes, challenge flawed assessments, and negotiate directly with the insurance company using evidence-based arguments. This relieves homeowners of the stress and ensures the insurer follows policy guidelines.

Perhaps the most valuable benefit is strategy. Professionals know when to push back, when to escalate the claim, and how to use documentation to challenge denials. With strong advocacy, homeowners often recover significantly more than they would on their own.

What Homeowners Should Do Immediately After Storm Damage

The steps homeowners take immediately after storm damage can dramatically affect the outcome of the insurance claim. Acting quickly and documenting thoroughly protects both the property and the right to compensation.

Safety comes first. Homeowners should stay clear of unstable roofs, broken glass, fallen trees, or exposed electrical wiring. Once safe, they should begin photographing damage from multiple angles before making any temporary repairs.

Temporary measures—such as covering holes with tarps or boarding broken windows—should be taken to stop additional damage. Insurance companies require homeowners to mitigate further harm, and failure to do so can reduce coverage.

Homeowners should save all receipts related to temporary repairs, hotel stays, meals, or emergency services. These may be reimbursable under additional living expense coverage.

Finally, homeowners should be cautious about giving statements to insurance adjusters before understanding the full scope of the damage. A single inaccurate phrase—such as estimating when the damage occurred—can lead to disputes or reduced coverage.

Conclusion

A storm damage insurance claim can be overwhelming, especially when dealing with structural losses, personal property damage, and the emotional stress of a severe weather event. Insurance companies often undervalue storm claims through rushed inspections, selective coverage interpretations, and aggressive depreciation. Homeowners who understand the claim process—and secure expert help when needed—are far more likely to receive fair settlements.

With strong documentation, accurate repair estimates, and professional guidance, homeowners can recover the full value of their storm damage insurance claim. A properly managed claim restores the property, protects the family's safety, and ensures long-term structural security.

.svg)